Join investors, institutional allocators, family offices and those who want an edge in private equity by subscribing to Letter Capital here:

The quaint city of Kristiansand is at the southern tip of Norway. The city centre can be walked in no more than 15 minutes, ending at Fiskebrygga, the harbour filled with fantastic seafood restaurants and locals soaking up the summer. In winter, the lakes freeze solid and the surrounding paths offer the best cross-country skiing anywhere in the world.

The economy supports some of the best in engineering innovation and industry. Work-life balance is a reality, not a platitude. Despite the eye-watering cost of a beer, Kristiansand is an idyllic spot to make a living.

Idyllic (before cost of beer)

Norwegian Access and Skill

Kristiansand is a microcosm of Norway and its economy. Kristiansand bats above its average compared with similarly sized cities, as does Norway on the global stage. Norway has the sixth-highest GDP per capita in the world. Its sovereign wealth fund has over US$1 trillion in assets (almost $200,000 per citizen), including more than 1% of all listed equities in the world.

This wasn’t always the case. Two things altered Norway’s future: access to the vast oil reserves in the North Sea and superior skill in extracting that oil. For decades, Norway represented the best of offshore technology and this has translated across other industries like energy, infrastructure shipping and aquaculture. Without both access to the best and superior skill, present-day Norway would be very different.

To replicate this is hard. There are limited unexplored and unlicensed reserves in the world (driving frontier exploration in places like the Arctic and technologies like fracking) and skill is developed through a complex combination of innovation, relationships and experience.

Private Equity Access and Skill

Norway is held as an example for preserving wealth and earning a decent return on that wealth. Its admirable performance is often pointed to as an example to follow. But without the same access and superior skill in something very specific, results will disappoint.

The long bow I’m drawing between Norway and private equity is this: without genuine access to the best private equity investments and superior skill in selecting those investments, returns will disappoint. This applies to both investing in funds and direct investments in the underlying companies. David Swensen, the CIO of the Yale University Endowment, describes this using venture capital:

Top-tier venture capitalists benefit from extraordinary deal flow, a stronger negotiating position, and superior access to capital markets.

Earnings Power

To understand why skill in private equity is important, we examine firstly, why equities outperform other assets like bonds, and secondly, the ‘alpha’ found in private equity.

The prevailing wisdom is that equities generally provide a higher return than less risky asset classes. The ‘equity risk premium’ is the difference between the expected return of equities over a theoretical risk-free return (a government bond is the common marker of a risk-free return). For almost a century, reality has matched the theory. Jeremy Siegel explains in his book ‘Stocks for the Long Run’:

Despite extraordinary changes in the economic, social, and political environment over the past two centuries, stocks have yielded between 6.6% and 7.2% per year after inflation in all major subperiods. The long-term perspective radically changes one’s view of the risk of stocks. The short-term fluctuations in market, which loom so large to investors, have little to do with the long-term accumulation of wealth.

Why is this so? The textbook answer is that returns must be higher to compensate investors for the additional risk. But how do stocks compensate investors? How do they offer higher returns? Simply put, equities can offer higher returns because they have Earnings Power. Cash generated by a business can be reinvested into that business to earn even more returns in future. Returns can compound. If you want to maximise long-term returns, there are few better options than equities.

Private equity can earn this same equity risk premium and then some. The ‘and then some’ is the partly apocryphal statement that private equity outperforms public equities with less volatility and less risk.

Why is this so? Inefficiency and owner-orientation. The latter is often written and spoken about: privately held businesses can have better alignment between the managers of the business and its investors. However, I think inefficiency is a more important and less understood reason why private equity can outperform.

Inefficient Markets

To start with, there is no handy list of the universe of businesses you could invest in, with prices, annual reports, list of directors and shareholder activity. The universe is large, larger than publicly listed business, but it is opaque. A list needs to be handbuilt. Calls need to be made, meetings (or beers) with management, negotiations on price and control. All of this is played out in an emotional environment with significant information asymmetry (the company will know more about its operations than the investor, but the investor might know more about the potential and worth of those operations). The rewards will accrue disproportionately to the private equity fund or manager with skill.

All else being equal, an inefficient market, like private equity, has a higher dispersion of returns and therefore more opportunity for outperformance resulting from skill.

I’m paraphrasing Brent Beshore:

Skill requires volume (and breadth) of experience and relationships.

Winners and Losers

Since dispersion is wide in private equity, LPs and capital allocators must have access to and select for skill when investing in managers. The average return will disappoint. As pointed out by Swensen, if there was a private equity index, the returns on that index would be reasonable at best, and probably poor after fees (except some highly inefficient niches within the asset class, a chat for another time).

Access to, and selection of, the best performing funds and investments in private equity is an opportunity for outperformance with less risk (i.e. ‘alpha’ allocation).

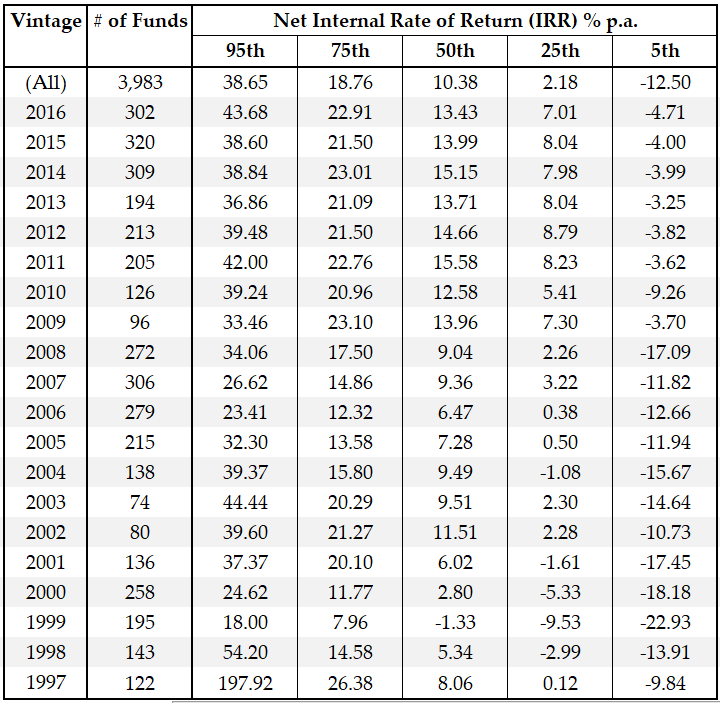

These ‘best performing funds’ can be thought of as the top quartile (or even higher) in that asset class, globally. To illustrate, let’s take 3,983 funds around the world, investing from 1997 to 2016 and split the returns into quartiles:

Source: Burgiss

If you had access to the top managers and enough skill in selecting those managers, you’d have done very well (19% net for the top quartile and a whopping 38% net for the top 5%). It’s no surprise the top performers are, well, top performers. It’s the dispersion that’s important. The median fund returned 10% - hardly exceptional given the S&P 500 returned about 8% during this time.

Seeing Around Corners

Another thing often missed by investors is that the winners not only make good money within private equity, but they have uniquely mitigated risk across other, usually larger, asset classes in their portfolio. Private equity is a “lens into disruption” as Mark Machin, CEO of the CPPIB, touches on this in this short interview (along with the importance of skill).

Asset allocators whose primary goal is to preserve wealth (e.g. a large family office) may even shy away from private equity because they believe it is an exclusively higher return/higher risk strategy. What’s missed here is that they might end up with more portfolio-wide risk by not exposing themselves to emerging technology and business models affecting the entire spectrum of assets under management.

An old and extreme example is Amazon - only a handful of investors as early as 1996 had direct, intimate knowledge of the huge disruption one company was unleashing on retail (notably, the VC firm Kleiner Perkins).

Finding Alpha

There are a fortunate few LPs and allocators who benefit from both high returns and insights that can be applied to their other asset classes. ‘Fortunate few’ since access remains the challenge. Again, Swensen describes it best:

All the top-tier partnerships limit assets under management and none of the top-tier partnerships currently accept new investors. Consequently, outsiders remain outside, limiting the available set of choices for new investors hoping to enter and existing investors hoping to upgrade.

Since the available opportunities for the overwhelming number of investors exclude top-tier firms, returns expectations require a commensurate downward adjustment. The inability to access the venture elite drives the final nail in the coffin of prospective venture investor aspirations. Exclusion from the venture capital elite disadvantages all but the most longstanding, most successful limited partners.

With both longstanding access and skill, it is no surprise Swensen’s Yale Endowment has achieved returns of over 30% per year in private equity from 1978 to 2007.

Before wading into the promising waters of private equity, make sure you have access to the most skilful managers. If not, you can get burnt with average returns. Almost as burnt as I did in Norway paying for a round of beers.

Never cross a river if it is 4 feet deep, on average - Nassim Taleb